These are the top 7 questions people ask when trying to begin their financial journey. Let’s take a look at them!

What is Compound Interest?

If there is one top 7 question topic you take away from reading here today, please let it be the idea of compound interest. With regards to saving and investing, it is the most important thing.

Compound interest is the idea of money earning money.

When an investment is allocated, it is started with a certain amount of funds. Those funds begin earning interest and the interest is paid. The interest can be compounded with different timings ranging from annually, to quarterly, daily, or even continuously.

When the interest is paid, the new amount in the account becomes the starting funds, plus the interest.

Over the next interest period, the funds then begin to earn interest based on this new amount – the funds plus the interest. In other words, the interest then begins to earn interest.

This is the power of compound interest.

In the form of investments, the idea is the same, it is just called compounding or compounding returns.

Why is this so important? The earlier you understand this concept, the sooner you will begin investing.

Over time, money can earn returns on itself. Starting earlier means there is more time for the interest to be compound. Which often means more money.

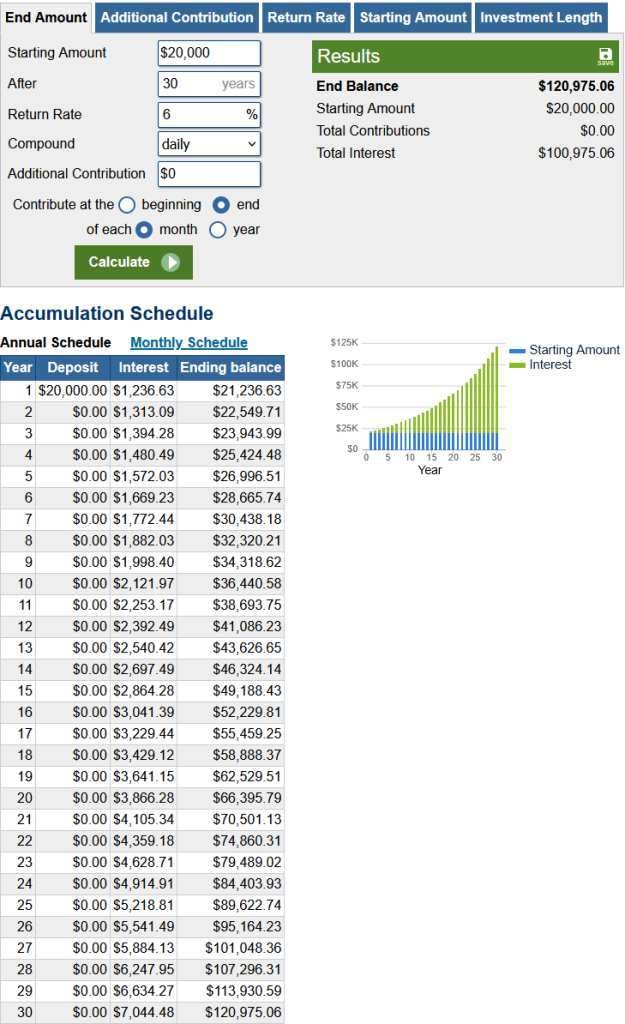

To give an example, here is an investment returns calculator from www.calculator.net

This example shows a starting initial investment of $20,000 earning the average return of the S&P 500 of 6%, every year for 30 years, with no additional contributions, and compounded daily. The ending result, simply for having started 30 years early and investing nothing else, is an ending balance of over $120,000.

This is the power of compounding returns over time. Learn this concept as it will serve very well to know it.

Save Money or Invest Money?

These goals go hand in hand and are not mutually exclusive.

Start with an emergency fund with a short term goal of $1000.

Then you can consider investing whilst balancing a

longer term goal of 3-6 months of monthly expenses.

Aim to invest money in tax sheltered accounts such as a company 401k or Roth IRA to save on income taxes.

The amount you invest does not have to be large and will likely vary from person to person, but the sooner you start and more importantly the sooner you make this process automatic, the sooner you can capitalize on compound interest and reliable savings!

Where do I save?

Try a High Yield Savings Account (HYSA).

If you’ve heard of a certificate of deposit (CD) a HYSA is similar.

A CD offers a set interest rate in exchange for a set time frame to maintain the money with a financial institution.

A HYSA does not offer a set interest rate, but instead allows funds to be withdrawn without a penalty when necessary.

These accounts have fluctuating interest rates that are significantly higher than traditional checking or savings accounts. Interest rates trend the market but have been as high as 4.0% or more in 2025.

This is a good place to keep an emergency fund. You can withdraw it when an emergency happens without penalty but the interest rate will hopefully allow the money to trend inflation so it does not lose it’s value by sitting in an account.

Where do I invest?

Long term investments for retirement are often in tax sheltered accounts such as the 401k or 403b, Roth IRA, or HSA.

Individual taxable brokerage accounts can also be opened at any time, however they are subject to taxes and rules for investment.

Some popular investment companies include:

- Fidelity

- Vanguard

- Goldman Sachs

- Edward Jones

- Charles Schwab

Each company comes with pros and cons and this is not an exhaustive list. It is worth it to do your research prior to deciding a company to invest with.

Some common things to look for are:

- Are some investments available or not only at a specific company?

- Do I know a company that is affiliated with one of these companies that I trust?

- Is my company sponsored retirement account already affiliated with one of these companies and do I want to keep everything at one place?

It is not necessary to be rich to start investing. Start small, but start, and remember, investing inherently has risk. Only invest what you can afford to possibly lose.

How do I save for retirement?

As mentioned previously, aim for a tax sheltered account such as a company sponsored 401k or Roth IRA. This can aid lowering taxable income.

If an employer offers a 401k match (which is an amount an employer puts into a 401k on behalf of the employee) contribute the amount necessary to gain the match*.

*As a note, company match often has a vesting schedule.

This means there is a time frame for how long until the money is officially the employee’s. The money will sit in the employee’s 401k account regardless of if it is fully vested or not. However, after this time frame, the money officially belongs to the employee.

A vesting schedule will be included with the description of a company 401k match plan.

Roth IRA are tax sheltered accounts which are owned by individuals. There are yearly contribution limitations. The interest and investment gains from this account are withdrawn tax free after maintaining the account for 5 years (as in the first year of your first contribution to the account, to the fifth year), and you reach 59 ½ years of age.

Please see the Roth IRA page for more information 🙂

Payoff Debt or Save Money?

Very individualized question. However the answer is rarely often one or the other, it is usually a combination of both and psychology is a very powerful influencer for individuals’ money choices.

Initially there is a price to be put on peace of mind. Saving a small emergency fund in order to alleviate the month-to-month money stress of paycheck in and paycheck out.

When you have $1000 put away to be covered the next time your washing machine breaks down, psychology can take a little bit of a step back.

Next, it may be wise to look at the compounding interest rate in versus the compounding interest out.

Does your 4% HYSA savings make sense if you are paying a 22% interest on credit card payment?

Does the compound interest on your investment exceed the compound debt that you have? If the answer is no, it may be worth reevaluating current planning.

Buy vs Rent

This example pertains to a home, but the rationale can be applied to other large purchase items.

Whether renting or buying, most people consider monthly payments should not be over roughly 30% of your gross monthly income.

Renting is a very good short term option. It allows an individual the flexibility of location and movement. If an individual is uncertain of where they wish to live, or what type of living space they wish (be it townhome, condominium, or family home etc.) renting can give insight into these situations and allow for wiser choices. However, price is also not controlled by the individual when renting. It is the largest cost of most peoples’ expenses, and it would be out of the control of the budgeter.

However, very savvy individuals will also consider the final price of the home.

How much will you pay over the lifetime of your mortgage?

Will a 15 year mortgage be more money or less than a 30 year mortgage in the long run?

As a rule of thumb, usually if the monthly payment is lower, the amount paid over the lifetime of a loan is higher. There are exceptions to this, for example – if the interest rate is reduced.

As an example:

Say there is a $450,000 home with mortgages offered over 15 and 30 years both with 20% downpayment, and a 6% interest rate.

Monthly Payments:

15 year: $3037.88

30 year: $2158.38

Total paid:

15 year: $546,819.22 (interest paid: $186,819.22)

30 year: $777,017.48 (interest paid: $417,017.48)

This is a gross oversimplification as usually lower term loans will have lower interest rates, no HOA is included, and a 20% downpayment also alleviates the requirement of mortgage insurance. But, it is wise to consider not only monthly payment, but total cost. The cost of interest over time, is compounding interest. We’ve talked about how it can benefit you, but this can also benefit businesses who give out loans too!

Whether to rent or own is a very complex topic and is an extremely individual choice to make. But now we have more tools to consider when we make the next decision.

Hopefully this helped you! Do your research, learn something new, and start your financial journey today!

From my mind to yours!

~Jay

I enjoy sharing what I have learned through my own personal finance journey!