Financial planning at any stage is difficult. Let’s discuss steps to take to improve your personal financial health!!

Six Steps to Financial Health

People do not often know how to begin on their financial journey. Money is a tool. Managing and learning to use it takes practice. For me personally, I started with a checklist to set me on the right track and to try and figure out where I was on the timeline of financial health.

- Budgeting

- Emergency Fund

- Start Retirement Investment (401k Match)

- Debt Payoff

- Refining Investment (IRA, HSA, Taxable)

- Personal Financial Goals

Budgeting

This is the beginning step. It’s also the step most people tend to skip. Do not skip this step it is so important!

The goal is to get solid information for your general spending habits as well. You can either gather the most recent three months of your financial information or begin RIGHT NOW and write everything down for the next three months.

The things which should be tallied are things such as:

Any income you make.

Any amounts you spend.

We do this to track the amounts we are spending. Most people have difficulty sticking to a specific budget, so this is to see what you spend and where. The goal is only to see what you are doing and understand where every dollar you have is going.

Is anything particularly high which could be lower? Are you ordering food really commonly because you are tired after work? Are you spending a large amount on a car you might not need? Is your home within your budget or stretching you too thin? It is so challenging to answer these questions without seeing a collection of your own personal information right in front of you to prove it to yourself. If you feel this helpful to continue doing, continue to do it. If not, then start doing it for a baseline so you know your big ticket items and understand where you stand currently. Setting up a three month budget and really take a look at how you are spending.

If this seems tedious to you, after three months you can set categories of finances instead of playing with spreadsheets forever. I personally love spreadsheets and seeing how I grow from month to month, but it is not the only way.

After three months you can try categories instead:

What do I need?

What do I save?

What can I spend?

These categories will help separate finances to help save money in different places and prepare for investment!

Okay! Now the hardest part is over. The progress starts now!

Emergency Fund

An emergency fund is savings earmarked for emergencies. Your car broke down. Your laundry machines need to be replaced. The roof is leaking. You have to move RIGHT NOW because your landlord is raising rent. An emergency room visit. You leave a job and have to look for a new one. This account is not for impulse shopping, pizza delivery, or ice cream/movie night.

The emergency fund should be in a savings account, often a High Yield Savings Account (HYSA). A High Yield Savings Account pays small interest on the funds in the account for keeping money in the account – more than a traditional savings account. The purpose of this interest is to keep up with inflation so your money stays as valuable as it was when you put it away, not necessarily to make money.

The purpose of this is to keep it liquid – to keep it available readily and accessible if needed when emergencies happen. My account is at a separate institution than my main checking account, but is still able to be accessed by transfer within one to three days.

This emergency fund can start small but the most important thing about it is it should be automatic.

Take a small portion of your paycheck, even if it’s $20, and auto allocate it through direct deposit into your savings account.

Focus on the initial goal of $1000. This is enough to solve most home appliance troubles and small car issues.

Your final goal for this account should be 3-6 months of all of your monthly expenses in this savings account. Some people have more, all the way up to a year’s worth expenses, but 3-6 months gives a lot of breathing room for most emergencies.

Start Retirement Investment

Okay. First thing with investments – many people do not invest because they are afraid of a market crashing. I want to address this concern first and right now.

The United States S&P 500 has an average rate of return of 6-7% per year when adjusted for inflation.

What does this mean? Over the time of the entire stock exchange gains on money in the top 500 companies in the country gain a value of 6-7% on the money per year. This is an average, meaning one year you may lose money but the next year your money will gain significantly. It will average out as a gain.

Waiting to invest because of fear of losing money does not trend with the entire history of the U.S. exchange. Even during the lowest points, the money recovers. Stick with it. It is more important to invest for long periods of time than to gain quickly. Quick gains usually require much hiring risk, similar sometimes to gambling. Long term gains are an investment.

*steps off of the soap box* Now that’s out of the way!

The first investment that should be considered is guaranteed return investments. These are very rare and the most common one that most people know of are workplace retirement plans.

401k or 403b

These plans are so similar. The difference is what kind of company offers them. 401ks are more common for private sector employers. 403bs are only for government or non-profit employers.

If you have a retirement account with your workplace – usually a 401k or 403b, contribute the percentage of your yearly salary that your employer will match you. It is a 100% gain on your money simply for participating in the fund. Each company has a different contribution amount based on how much you are putting into the account and will be available information to you during open enrollment usually around november for the new fiscal year at a company.

Example: 6% of your income contribution with a 6% match from the company vested over three years.

Vested is a fancy term that means the company contributions become available to you in the time frame specified. In the example, the amount the company matches is yours after three years. You work for the company for three years and you own your entire 401k account permanently. Some companies vest immediately, but many do not.

This is the most basic form of investment. These plans are managed by the employer you have it with, but you are able to change where the money is placed if you wish to later. At the beginning, the plan will choose a fund which is marked for the year that you are going to retire based on age. The fund will be adjusted by the company fund owners to adjust the risk to lessen as you get older.

Debt Payoff

Okay, the hardest part for most people. We are not just saving, we are also needing to live somewhere. Go to school. Have expenses that surprise us. Therefore we have debt. Credit card debt, Student loans, Car loans – the type of debt is irrelevant. Let’s talk about debt payoff.

For the sake of debt payoff, we are excluding Mortgage payments because this is considered lower interest debt or long term debt which gains value. We are focusing on debt which is exclusively earning interest and therefore is only costing additional money in the long run.

There are two common ways of looking at debt payoff.

The Debt Avalanche Method

The first is looking at debt by interest rate. This is commonly referred to as the debt avalanche method.

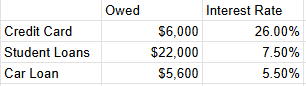

Sort your debt from highest interest rate to lowest interest rate.

This is the financially beneficial route if you are looking to pay the least over the shortest time. The goal is consistency! Pay the minimum amount to all debts, and pay any additional funds (after your emergency fund savings) towards the highest debt you have. In our example it would be the credit card debt at 26% (HIGH) interest. Even if it’s $5 more per payment. This is to pay off sooner than the current schedule of the loan.

As an interesting note: Most minimum payments on credit cards assume someone will be paying off the loan in ten years time, accumulating the interest for ten years.

The Debt Snowball Method

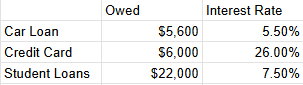

The second is looking at debt by the current amount owed. This is commonly referred to as the debt snowball method.

Sort your debt from the lowest total amount owed to the largest total amount owed.

The goal of this is to trigger our psychological wins with a dopamine rich brain! While this will end up being slightly more money than the other method, it is still a way to keep on track if the idea of paying by interest rate will deter you from sticking to the plan! Remember, the goal is consistency!

After you finish the first loan, take the amount you were allocating to the first loan and apply it to the next loan on the list. Eventually this will build a large payment towards the last debt using the previous debts money which you are already used to paying from your budget.

Refining Investment Accounts

With an emergency fund established, 401k match established, and debt payoff methods planned and underway, the considerations for more investment opportunities can begin!

There are multiple different accounts which can be used for this. Some are tax advantaged and others are not. These can be opened with a brokerage company online. Popular ones include Fidelity, Vanguard, and Charles Schwab.

Investment accounts allow you to save money for a later age. They are unique in that you can control how to invest your money. There are many different kinds:

- IRA

- Individual Retirement Agreement. An investment retirement account which is linked to an individual. The funds can be invested. There is a set amount that can be contributed to this account per year. I’ve written in detail about these accounts in another post. More about this account type can be read here

- HSA

- This is a Health Savings Account. You contribute funds to this account yourself. These funds are investable but the funds are only able to be used on Health adjacent items such as hospital visits, PCP visits, medications and prescriptions, among many other things. A complete list can be found online. This account requires enrollment into a High Deductible Health Plan (HDHP). This is a specific type of health plan which can be offered by employers (not always) but must fit set parameters for deductibles as described by the IRS.

- Brokerage

- No tax benefits, but completely available for withdrawal and investment at any time depending. Taxes on gains are assessed based on withdrawal from the fund invested into, not the account itself.

The most passive and basic type of investment is called “index funds”. These funds are collections created by brokerages which charge a very small percentage of the investment amount per year in order to maintain the investment in the account.

There is an S&P 500 index fund affiliated with most brokerages, at this time I know of one at both Fidelity and Vanguard. These funds trend the top 500 companies in the United States stock exchange and are manipulated by the brokerages as the companies in the top 500 change. This is what the small cost per year is for – to maintain the fund accuracy per the S&P 500 and to pay the individual managing it.

This is the most basic and passive sort of investment. I will cover more detail in further blog posts.

Personal Financial Goals

This is the time to start setting up your personal financial goals with additional savings accounts or retirement accounts.

Are you saving for a home down payment? Or a second home even?

Are you planning on having a child?

Are you going to get married?

This is the time to think on what comes next so the next time you have a big expense, you can pay cash for it

Interesting note: “Pay for it in cash” implies you have the money to pay for a big ticket item in an account before you buy it. It does not mean pay using only physical cash. Savvy individuals will use credit to pay for big ticket items on a credit card, and then immediately pay for that credit card the same month, prior to the next statement coming due. This prevents any interest from accruing, and allows you to accumulate the points on a good credit card for a vacation trip!

Hope something included here was informative and useful to you!

From my mind to yours!

~Jay

I enjoy sharing what I have learned through my own personal finance journey!